Articles · Research

One System of Record, Not a Stack of Tools: The Real Cost of Tool Sprawl in Venture

Why a generic CRM plus spreadsheets plus a shared drive quietly taxes a venture or private-markets firm — and what changes when sourcing, diligence, IC, and portfolio share one system of record per company.

Most venture and private-markets firms do not lose deals because they lack judgment. They lose them because the information needed to make a decision is scattered — pipeline in one tool, diligence notes in another, metrics in a third, and the actual reasoning in someone's inbox. Each tool is individually defensible. The stack is the problem. This piece is about the quiet tax that tool sprawl puts on a relationship-driven firm, why a general-purpose CRM rarely fixes it, and what a single system of record actually changes.

The quiet tax of tool sprawl

Fragmentation is not a venture-specific affliction; it is the default state of modern software operations. The average company now runs hundreds of SaaS applications — by one analysis around 275, with large enterprises running closer to 660 — and the bill is not only the licenses. As Syncro's breakdown of the true cost of IT tool sprawl notes, the larger, hidden cost is reconciliation time across disconnected systems, the maintenance of the connectors that stitch them together, and the context-switching that fragmentation forces on the people using them — which research suggests can consume up to 40% of a knowledge worker's productive time. The same analysis cites IDC research suggesting that consolidating tools can cut tool-related costs by up to 30% and lift staff productivity by up to 25%.

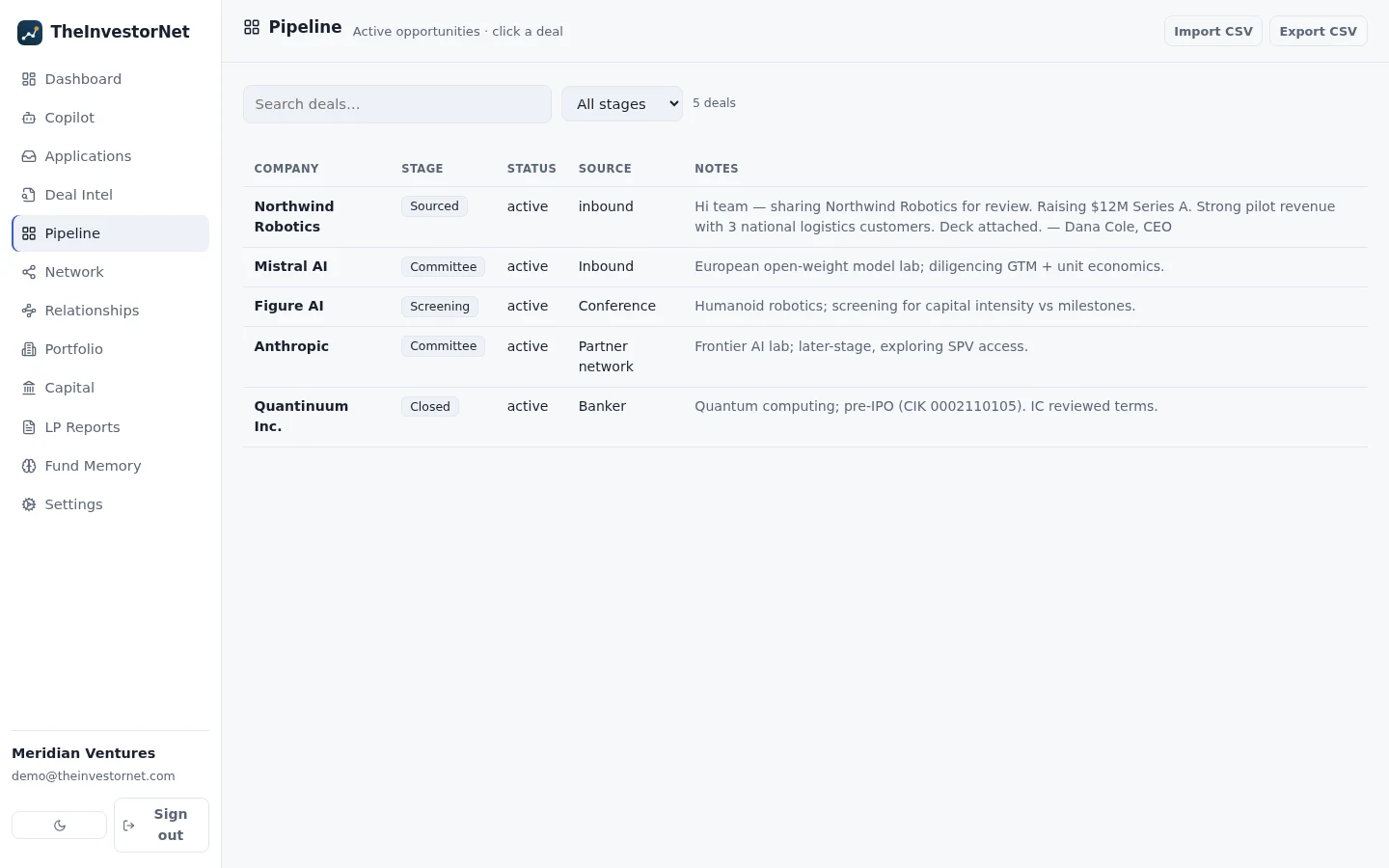

For an investment team, the sprawl shows up as re-keying. Assembling an investment-committee packet means copying a company's numbers out of a spreadsheet, its notes out of a CRM, its documents out of a shared drive, and its history out of email — by hand, every time. Industry analysts estimate that roughly 71% of applications in an average enterprise remain unintegrated, which means most of that copying is permanent, not a transition state. The work is invisible because it is spread across many small acts of reconciliation, but it adds up to partner time spent assembling the picture rather than acting on it.

Why a general-purpose CRM doesn't fix it

The instinct is to buy a CRM and call it the hub. The trouble is that CRMs are built for a different shape of work, and the adoption data is bleak. Across sectors, CRM adoption is famously low — multiple surveys put the share of sales reps who actually use their company's CRM well below half — and the systems impose real overhead: by one accounting compiled in CRM adoption research, the average rep spends roughly six hours a week on manual data entry. When a tool relies on diligent hand-entry to stay useful, it predictably decays. As Affinity argues in its case for looking beyond traditional CRMs, "the more it relies on manual intervention, the less likely it will be to remain up-to-date, accurate and useful."

There is a second, deeper mismatch. A traditional CRM models a linear sales funnel — a transactional relationship moving toward a close. Investing is not that. Affinity frames the distinction directly: relationship-driven firms have "relationships [that] are collaborative, whose workflows are unstructured," and a CRM built for sales "[doesn't] usually tell you much about the nature of the relationships you have" or how the people in your network are connected to one another. A generic CRM can store that a meeting happened; it is poor at capturing why a firm passed, what the diligence turned up, and how a warm path to a founder actually runs. This is why a category of relationship-intelligence tools — Affinity, DealCloud, and others — emerged specifically for capital-markets workflows: they are built around the relationship graph and the deal record, rather than the opportunity-and-quota model a general-purpose CRM like Salesforce assumes.

What "system of record" actually means

The term gets used loosely, so it is worth being precise. A system of record is, in IBM's definition, the authoritative source for a given piece of business data — the place that, by design, holds the validated version everyone else defers to. The point is not storage; it is authority. When a system of record exists, there is no ambiguity about which spreadsheet is current or whose inbox has the latest term sheet, because the record is the single point of truth and conflicting versions stop multiplying.

The modern VC/PE landscape is, in practice, a set of overlapping systems of record, each scoped to one domain. Carta is the authority for cap tables, 409A valuations, and fund administration; relationship-intelligence CRMs are the authority for the network and the pipeline. That specialization is genuinely useful — but it also means a firm can own several excellent systems of record and still have no single record of a company: its sourcing, its diligence, the IC decision, the rationale, and the portfolio metrics afterward, all in one place. The gap is not between "one tool" and "many tools." It is between many records of a company and one.

What consolidation actually changes

Consolidating onto a single record per company does not add features so much as it removes the re-keying and restores the firm's memory. Three things change concretely.

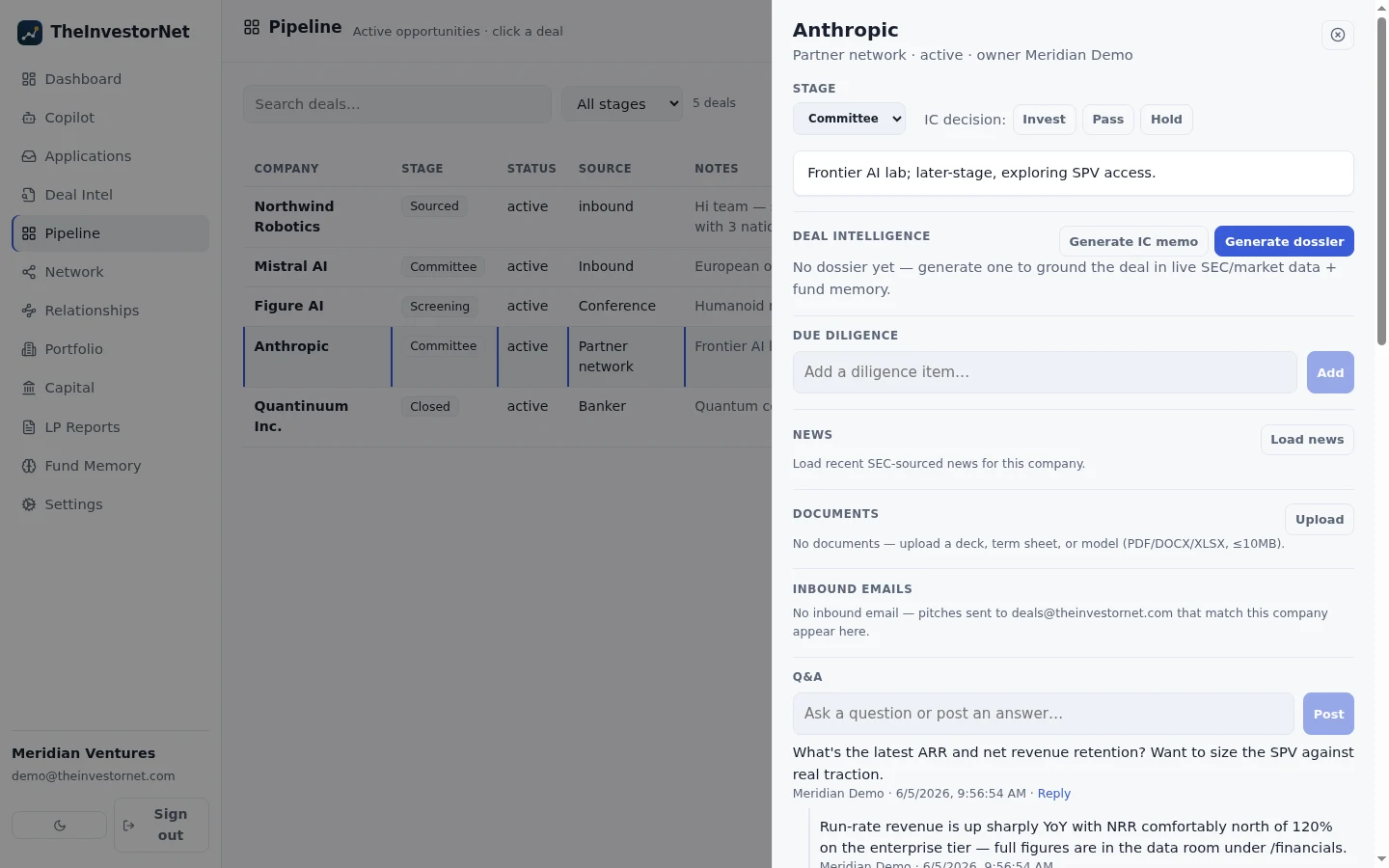

IC preparation gets faster. When intake, notes, stage gates, diligence evidence, and metrics already live against one record, the IC packet is a view of data the team has been maintaining all along — not an afternoon of copying between systems. The reconciliation tax disappears because there is nothing to reconcile.

Decision rationale becomes durable. The most expensive thing a fragmented stack loses is why. Six months after a pass, a firm with a real system of record can reconstruct what it knew, what it weighed, and what it decided — the diligence, the open questions, and the recorded reasoning all travel with the company. That is the institutional memory a CRM built for closing deals was never designed to hold.

There is one record per company, end to end. The story behind a deal travels with it from first email to board seat, and every stakeholder works from the same record, the same documents, and the same open questions — rather than from different versions scattered across handoffs.

This is also where consolidation compounds. Because the metrics that feed a quarterly review are already structured against each company's record, portfolio monitoring and LP reporting draw from the same source rather than a fresh round of collection — the analytics layer becomes nearly free. (For how to turn those structured metrics into earlier decisions, see our companion piece on data analytics for portfolio management.)

Further reading

- Syncro — The True Cost of IT Tool Sprawl (and What Consolidation Buys You)

- Clari — Why Your Sales Team's CRM Adoption Is Low

- Affinity — Looking Beyond Traditional CRMs to Develop Relationship Intelligence

- IBM — System of Record vs. Source of Truth

- Carta — The End-to-End Suite Connecting Private Capital