Articles · Research

Tech-Enabled LP Reporting: Metrics, Standards, and Making Reporting Nearly Free

A practitioner's guide to modern LP reporting: what limited partners actually expect, how to define DPI, TVPI, RVPI and net IRR precisely, the ILPA Reporting and Performance Templates, sensible cadence, and how reporting becomes nearly free when it rolls up from a system of record you already keep current.

Limited partners rarely fault a manager for a hard quarter. They lose confidence when reporting is late, inconsistent, or hard to reconcile — when the DPI in the quarterly letter doesn't tie to the capital account, or when "net IRR" means something different than it did last year. Good investor relations is, at bottom, an operations problem: define the numbers precisely, report them on a predictable cadence, and make the package fall out of records you already keep current rather than assembling it by hand each period. This is a practitioner's guide to doing that — what LPs expect, the metrics that carry the weight, the standards worth adopting, and why the marginal cost of a report should approach zero.

What LPs actually expect: transparency, consistency, timeliness

Institutional LPs are not asking for more pages. They are asking for three things, in order.

Transparency — enough detail to independently verify performance and understand where fees, expenses, and carried interest went. The line items should reconcile to the financial statements, not to a marketing narrative.

Consistency — the same metrics, defined the same way, in the same layout, every period. A trend is only readable when the definition behind it doesn't move. The single most common reporting complaint from allocators is not a bad number; it's a number that can't be compared to last quarter's because the methodology quietly shifted.

Timeliness — delivery on a predictable schedule. Industry practice for unaudited quarterly reporting clusters around 60–90 days after quarter-end, with audited annual financials typically within 120 days; ILPA's principles push managers toward the faster end of that band, and best-in-class shops deliver well inside 60 days (Carta's overview of investor reporting walks through the typical calendar). For most LPs, predictable matters more than fast — they have their own board and audit deadlines to feed, and a report that arrives on the same day every quarter is worth more than one that is occasionally early and occasionally three weeks late.

The metrics that carry the weight

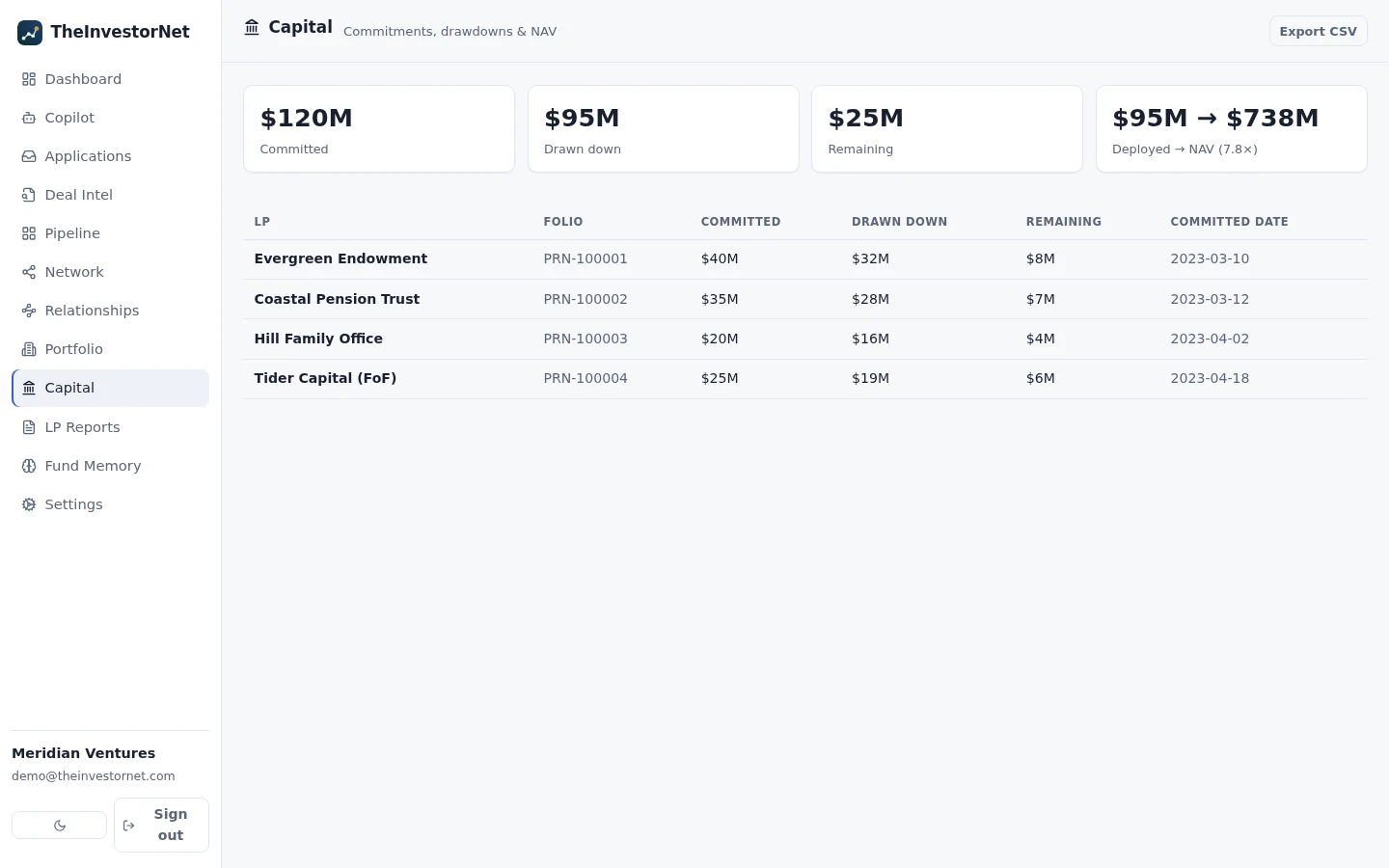

Four numbers do most of the work in an LP report. Three are multiples — simple ratios of value to the capital LPs paid in — and one is a time-weighted-for-cash-flows rate. Define each precisely, because the precision is the credibility.

-

DPI — Distributed to Paid-In. Cumulative cash (and stock) distributions to LPs divided by cumulative paid-in capital. DPI is the most concrete multiple because it counts only what has actually left the fund and reached investors — no marks, no estimates. A DPI of 1.0x means the fund has returned all the capital LPs contributed; above 1.0x is realized profit. In a slower exit environment, allocators have increasingly treated DPI as the metric that separates real returns from paper ones (see BIP Ventures on TVPI, DPI and IRR).

-

RVPI — Residual Value to Paid-In. The fund's remaining (unrealized) net asset value divided by paid-in capital. This is the part of the return that still depends on your valuation policy and on exits that haven't happened yet.

-

TVPI — Total Value to Paid-In. Realized plus unrealized value over paid-in:

TVPI = DPI + RVPI. It is the headline "how much value per dollar in" figure. Read it together with DPI: a 2.5x TVPI that is 0.3x DPI and 2.2x RVPI is a very different fund from a 2.5x TVPI that is 2.0x DPI — the first is almost entirely unrealized marks. -

Net IRR — Internal Rate of Return, net to LPs. The annualized, cash-flow-timing-weighted return to limited partners after management fees, fund expenses, and carried interest. Net IRR is the figure LPs underwrite to, and the one ILPA-aligned reporting puts front and center. Always distinguish it from gross IRR (before fees and carry); the gross-to-net spread is where the fee load lives.

Multiples and IRR answer different questions and disagree on purpose. IRR rewards speed — returning capital early lifts it — while multiples ignore timing and measure magnitude. A fund can post a strong IRR off a quick early exit and a mediocre TVPI, or vice versa. Report both, and report them net. For the portfolio-company KPIs that feed these fund-level figures from the bottom up, see our companion piece on data analytics for portfolio management.

Adopt a standard: the ILPA templates

You don't have to invent a reporting format. The Institutional Limited Partners Association (ILPA) publishes voluntary, industry-developed templates that have become the closest thing private markets have to a common language — and adopting them signals to allocators that you report the way they want to consume.

Two are worth knowing:

-

The ILPA Reporting Template standardizes the disclosure of fees, expenses, and carried interest. First released in 2016, it was updated through 2024 and a version 2.0 was published in January 2025, adding more granular partnership-expense breakouts, explicit identification of amounts paid to the GP and related persons (internal chargebacks), and tighter alignment with general-ledger and accounting conventions.

-

The ILPA Performance Template, new in the same January 2025 release, standardizes return reporting — IRR, TVPI, and multiple on invested capital with designated gross and net breakouts, alongside the cash-flow and portfolio-level detail that supports them. It comes in two methodologies (a granular, fund-to-investor cash-flow version and a "gross-up," fund-to-investment version) so different fund structures can comply consistently.

Both were delivered through ILPA's Quarterly Reporting Standards Initiative (QRSI) and are positioned for funds commencing operations on or after January 1, 2026, with the updated Reporting Template replacing the 2016 version on a go-forward basis. Even if you adopt them only in spirit, they give you a defensible answer to "how do you define and present this?"

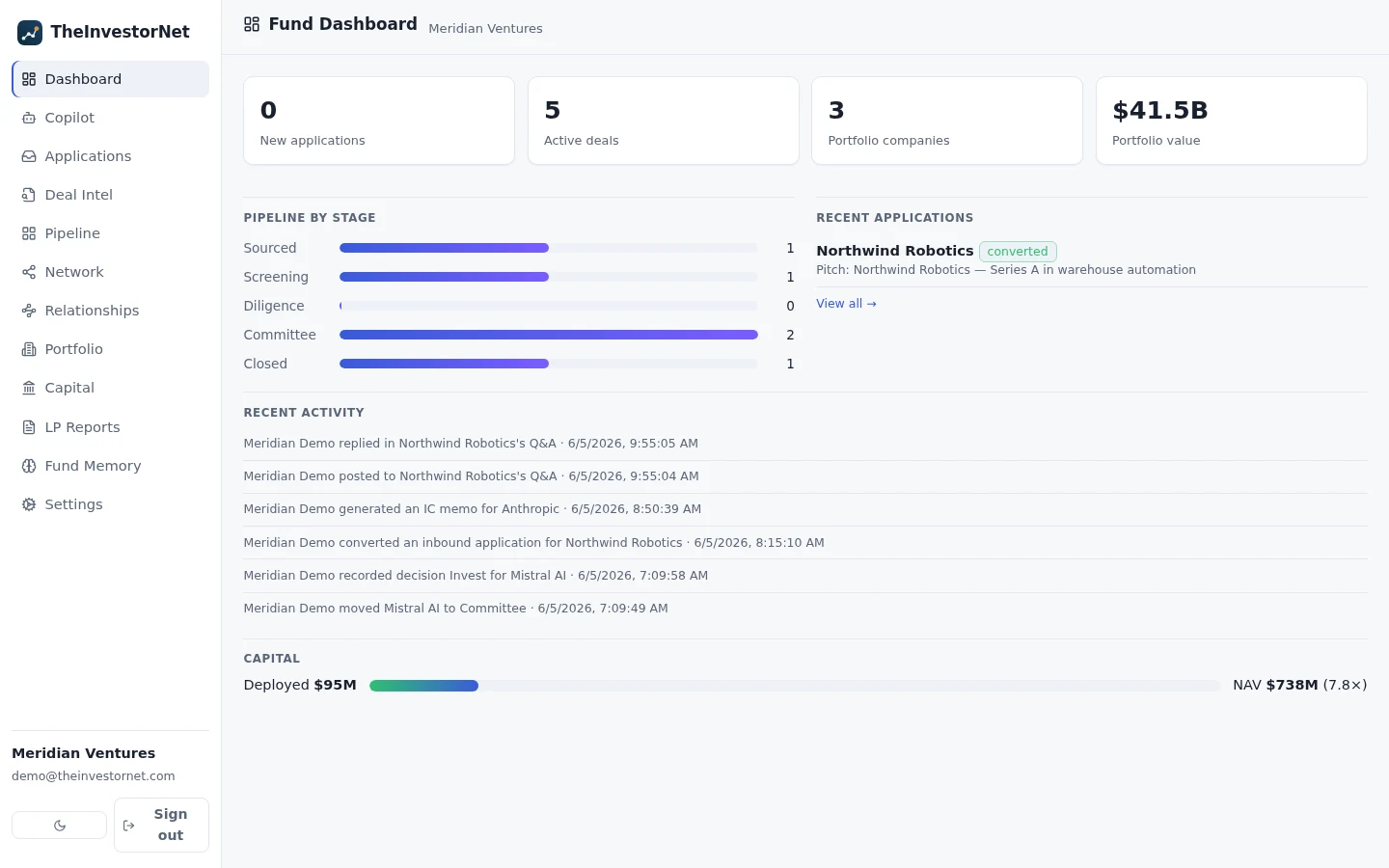

Reporting becomes nearly free when it rolls up from a system of record

Here is the operational thesis. Most of the cost and most of the errors in LP reporting come from one bad pattern: the data lives in scattered spreadsheets, inboxes, and a fund administrator's files, and each quarter someone re-assembles a package by hand — copying commitments, drawdowns, distributions, valuation marks, and KPIs into a fresh deck, then reconciling the inevitable mismatches. The report is expensive because it is reconstructed every period.

Invert it. If your commitments, capital calls, distributions, NAV marks, and portfolio KPIs already live in one system you keep current as a matter of running the fund, the LP report is no longer a construction project — it is a view. DPI, RVPI, TVPI, and net IRR are derived from the same cash-flow and valuation records that drive every other decision; the capital account ties to the ledger because it is computed from the ledger; the quarterly package is a rendering of state, not a fresh manual assembly. The marginal cost of the next report approaches zero, and — just as important — it is internally consistent by construction, because every number traces to one source.

This is also where transparency and consistency stop being aspirations and become defaults. Because the underlying records are the same ones used internally, there's no second set of books to reconcile; the LP sees a faithful projection of the fund's actual state, on the cadence you set, in the layout the templates define. The work shifts from producing the report to deciding what it should say — the commentary, the attribution, the forward view — which is the part LPs actually value and the part only a human can write.

What good looks like, in practice

- Write the definitions once. Net IRR net of what, TVPI on whose valuation policy, as of what date. Put it in the LPA-aligned reporting policy and don't drift.

- Adopt the ILPA templates — Reporting Template for fees/expenses/carry, Performance Template for returns — at least in structure, so allocators consume what they expect.

- Set a fixed cadence and hit it. Pick a quarterly delivery date inside the 60–90 day window, annual audited financials inside 120 days, and treat the calendar as a commitment.

- Keep one system of record current for commitments, calls, distributions, NAV, and KPIs — so the report is a view, not a rebuild.

- Spend the saved time on the narrative, not on reconciliation. The numbers should assemble themselves; your judgment is what the LP is paying for.

The funds that win the reporting relationship are not the ones with the prettiest decks. They are the ones whose numbers always tie, always arrive on time, and always mean the same thing they meant last quarter — because the report is a faithful rendering of a system they keep honest every day.

Further reading

- ILPA — Reporting Template (fees, expenses, carried interest)

- ILPA — Performance Template (IRR, TVPI, MOIC, cash flows)

- ILPA — announcement of the updated Reporting Template and new Performance Template (Jan 2025)

- Morgan Lewis — Fifth Circuit Vacates SEC Private Fund Adviser Rules in Full (June 2024)

- Carta — Investor reporting: from compliance to strategy

- BIP Ventures — Understanding TVPI, DPI, and IRR

- Related: Data analytics for portfolio management